ALUMAG® has analyzed the composite / carbon fiber threat against cast aluminum within suspension and BIW applications.

The main goal was to provide the client [European aluminum foundry] with an application overview outlining the composite / carbon fiber threat by means of a timeline “What to expect when”.

The timeline was based on existing ALUMAG® market information as well as on 20 interviews with industry experts representing OEMs, carbon fiber producers and tool makers.

–

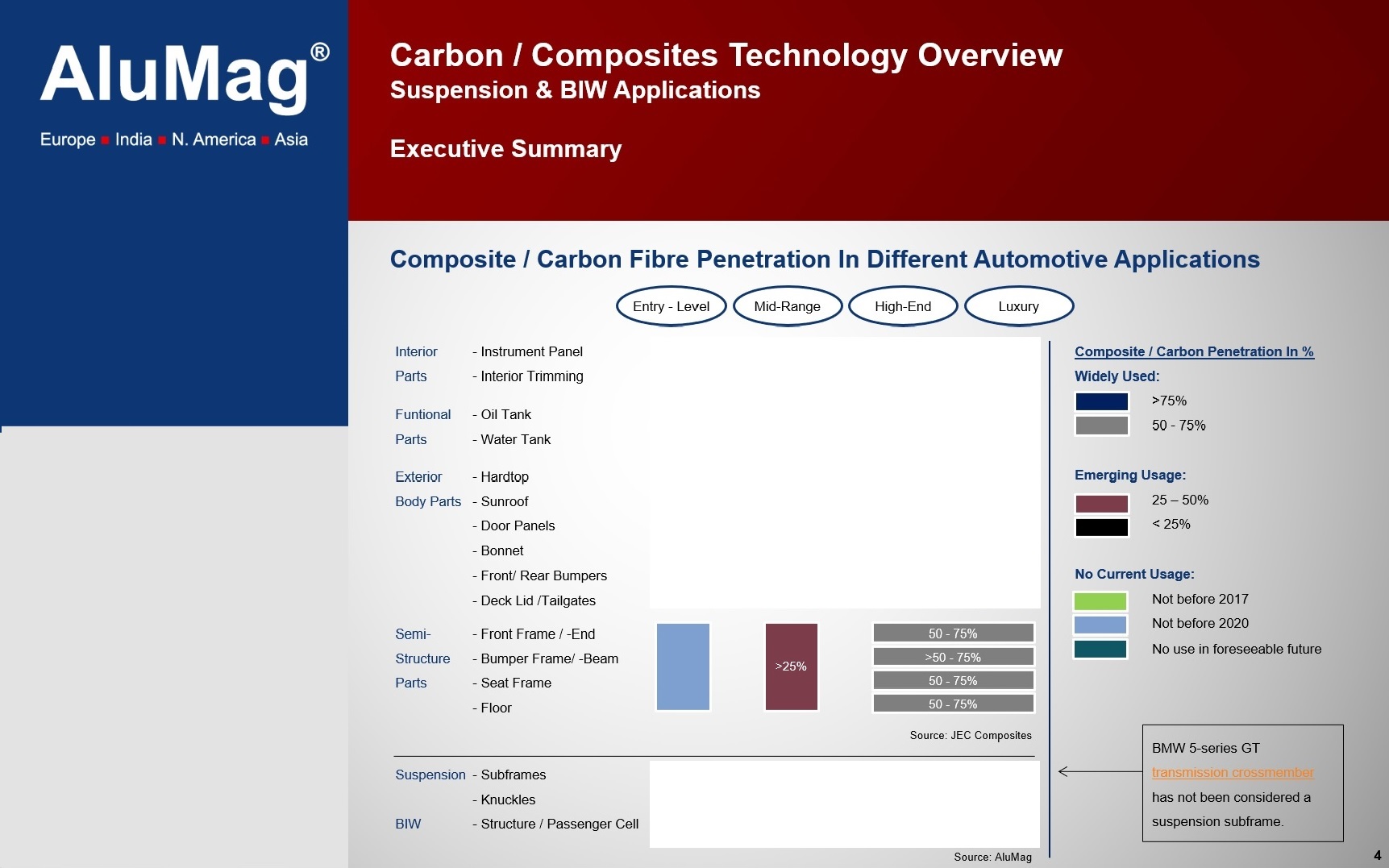

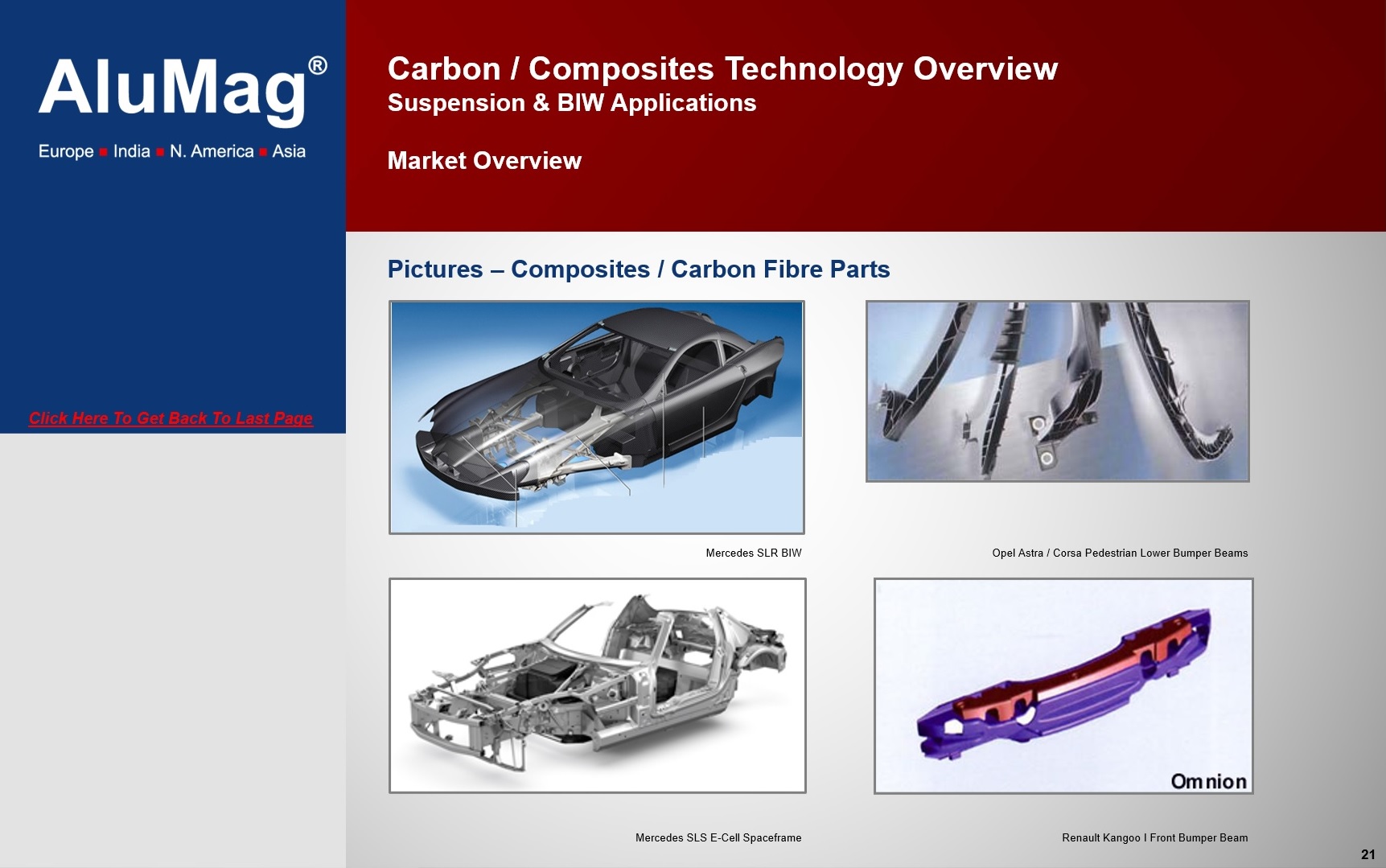

Samples of composite / carbon fiber automotive applications, source ALUMAG®

Cast aluminum is primarily used in power train applications, such as cylinder heads, engine blocks and transmission housings. In NA about 85% of all vehicles are equipped with an aluminum engine block. In Europe, this figure is 55%, 60% in China and 45% in Brazil [2015]. For 2020, a penetration rate of 89% in NA is expected.

Another important application is cast aluminum wheels, currently around 45% of all vehicles sold are equipped with original cast aluminum wheels world wide. In NA, the OE incorporation rate is of 77% [2015]. For 2025 OE penetration rate of 50% is expected worldwide.

When it comes to BIW structures, especially sports cars are equipped with cast aluminum [vacuum HPDC] since the 90s. Audi initiated the turn with the introduction of an aluminum frame for medium to high Volume vehicles [A8 and A2] beginning of this millennium. The Audi “space frame“ Was made of cast-, extruded- and sheet aluminum processed parts. With a very high growth rate of applications in the automotive structure, aluminum is no longer a rarity. New generations of models of high-end car manufacturers such as MB [C,E, and S-Class], BMW [X5, X6, 5 & 7-Series], JLR [Range Rover, Range Rover Sport, XJ, F-Type, XE] Cadillac [ATS, CTS, CT6], Audi [Q7, A4, TT, A8, A6] have ..

–

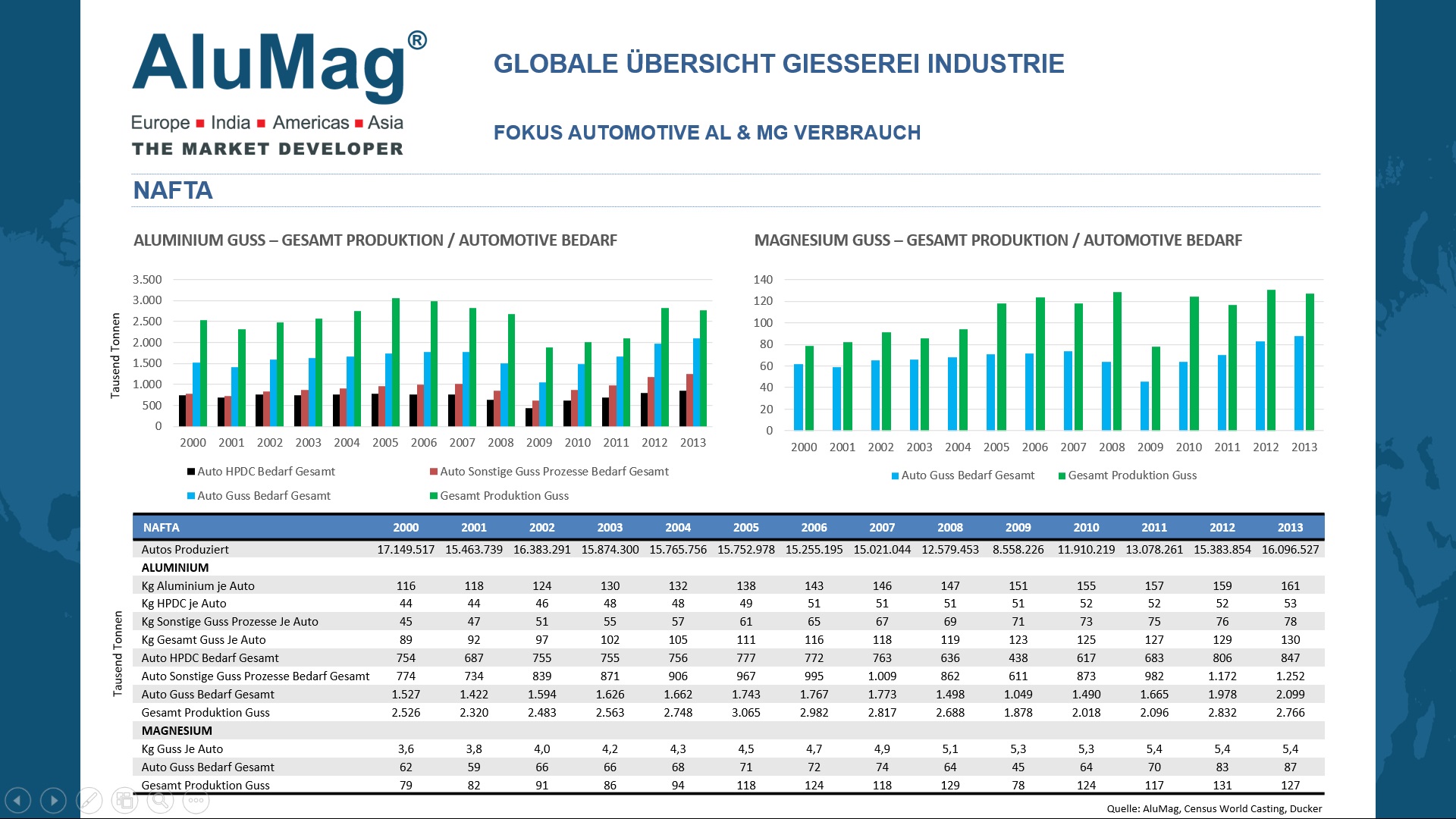

AL Cast Market Summary & Outlook NAFTA – Source ALUMAG®

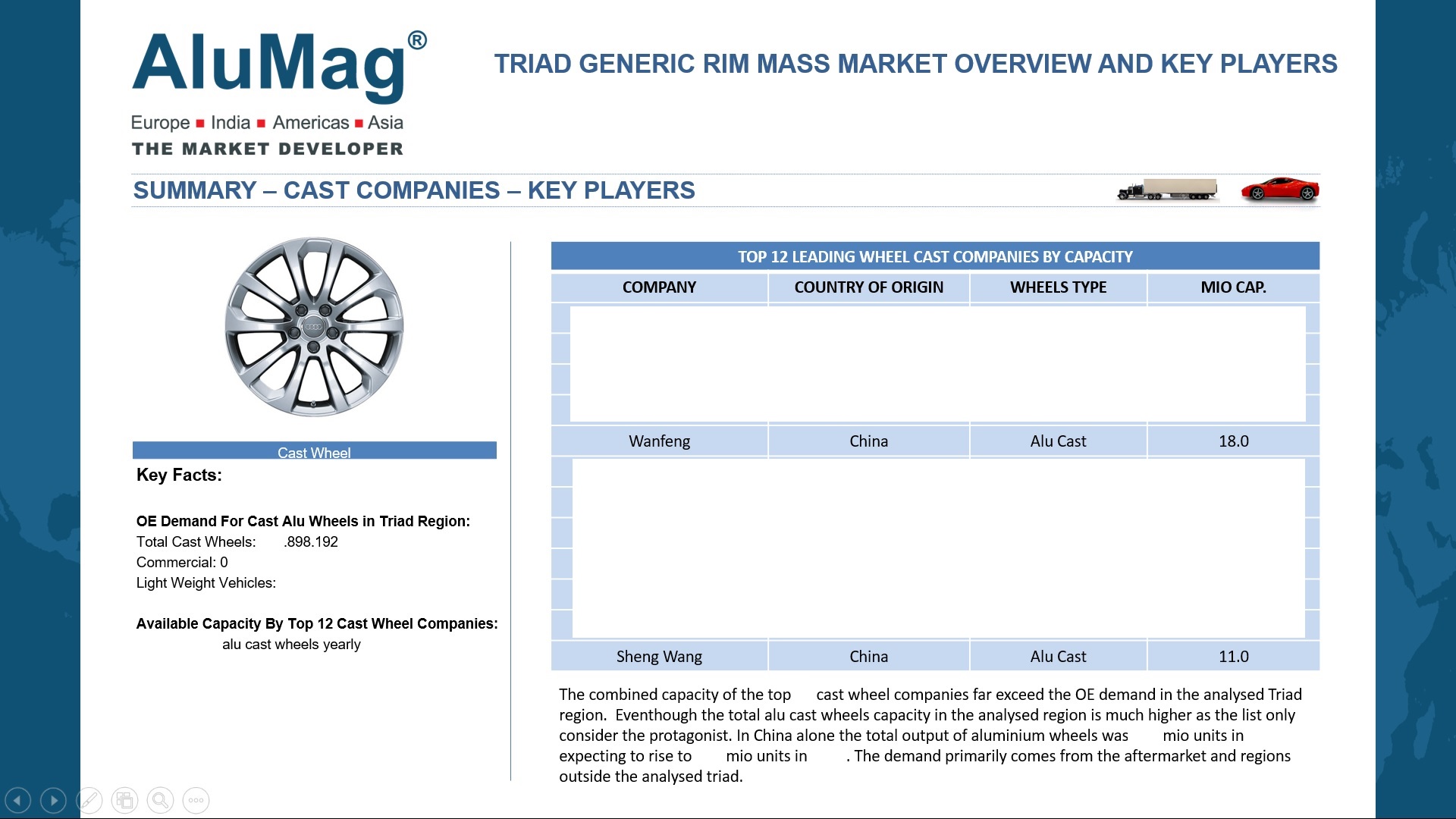

Worldwide the market for OE aluminum wheels is expected to grow with 0,91% in the period 2014-2015 within light weight vehicles. From 44% in 2014 to 45% in 2015. In the period 2014-2029 a growth rate of 7% points is expected which will bring the worldwide penetration of OE aluminum wheels up to 51% in 2029. The Highest growth rates in the period 2014-2029 are expected in China [14% points], Japan [13,5% points] and Central Europe [15% points].

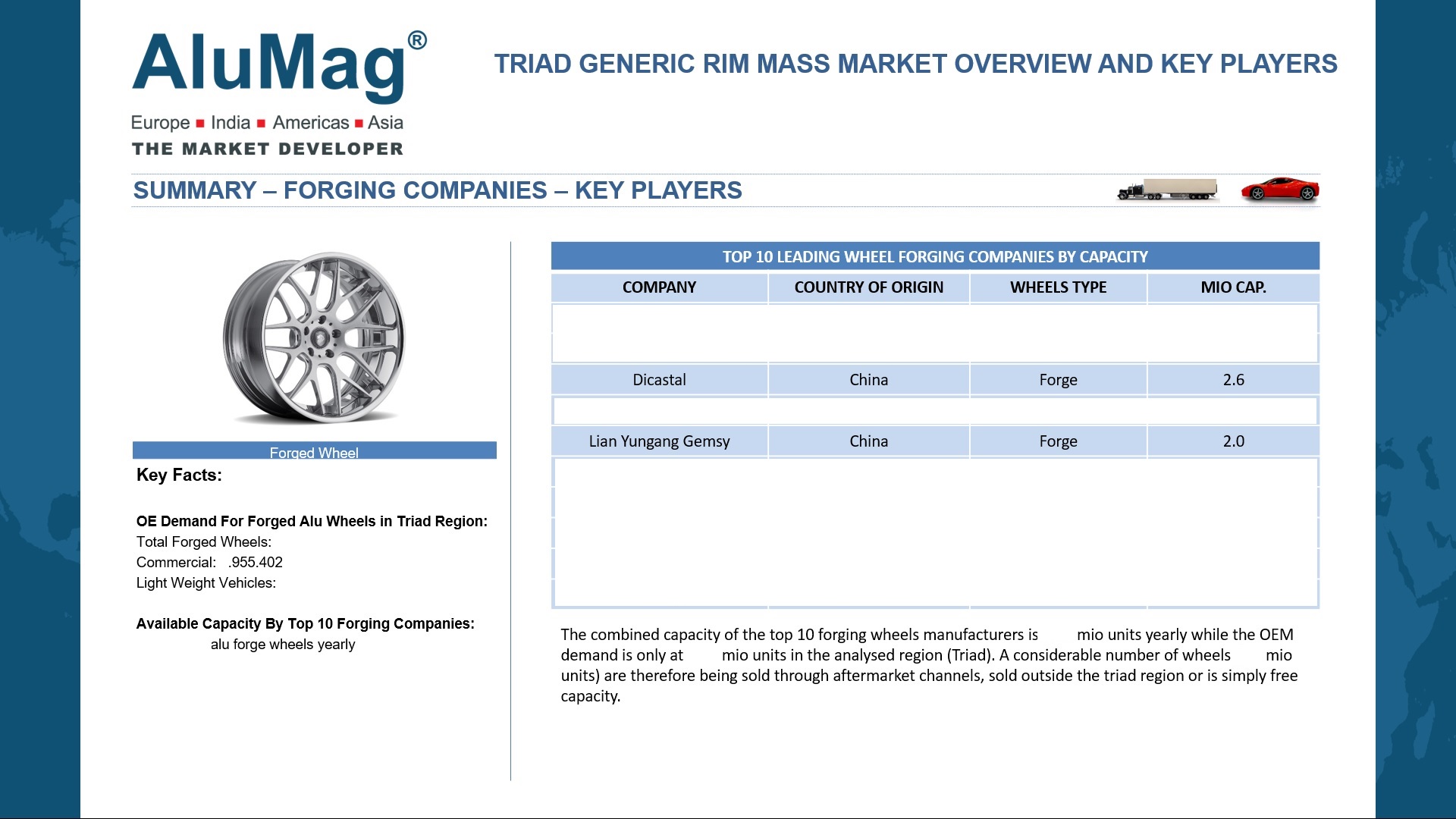

Cast wheels will remain the preferred alloy wheel for light weight vehicles while the penetration of forged wheels is expected to grow moderate over the coming years.

Today forged wheels are primarily used on high end vehicles and sports cars, but the booming electric vehicle segment Could boost the penetration of forging wheels in the near future. On the other hand new hybrid wheels to be launched by Maxion / Thyssen could become a threat to forging wheels manufacturers.

The penetration of forged wheels within commercial vehicles [Medium – heavy duty trucks, trailers and buses] is 13% on average in the analyzed regions. Again Nafta is the market with the highest penetration rate of forged wheels with 40%. Trailers and trucks in Nafta has in general more axles compared to other regions,..

Study was executed in year 2016/2017.

–

Global Forged Alloy Wheel Market Summary/Outlook – Source ALUMAG®

Within an overseeing period of time, client will run-out of orders for exciting process lines in the location XXX with casting cells in line and round tables

Client will get an entire overview about the market players and applications

Cylinder heads are not really in the clients focus. But, GDC & LPDC machines which are processing Cylinder heads today, could be used in future for any other products too. Means, this capacity / company will be looked at too

The research will consider entire Europe

The machines / area, which will run out of production, could be use with:

existing machines for new products

refurnished / modified existing machines for new products

new machines for new products

–

CSA [Former Georg Fischer] Overview – Source ALUMAG®

SCOPE:

GDC and LPDC including hollow cast and counter pressure in Europe 28

The client is a Japan based aluminum processing company and a leader in the industry. The client would like to get a sustainable understanding and benchmark of the global industry leaders like; Nemak which specializes in the production of cast aluminum powertrain components such as cylinder heads, engine blocks and transmission parts for light vehicles. Since the cast structural “body in white” [BIW] will be applied for areas where strong part integration is feasible, Nemak is going to target new components / areas like thin-wall, ductile and weldable castings. This is a target market for the client too.

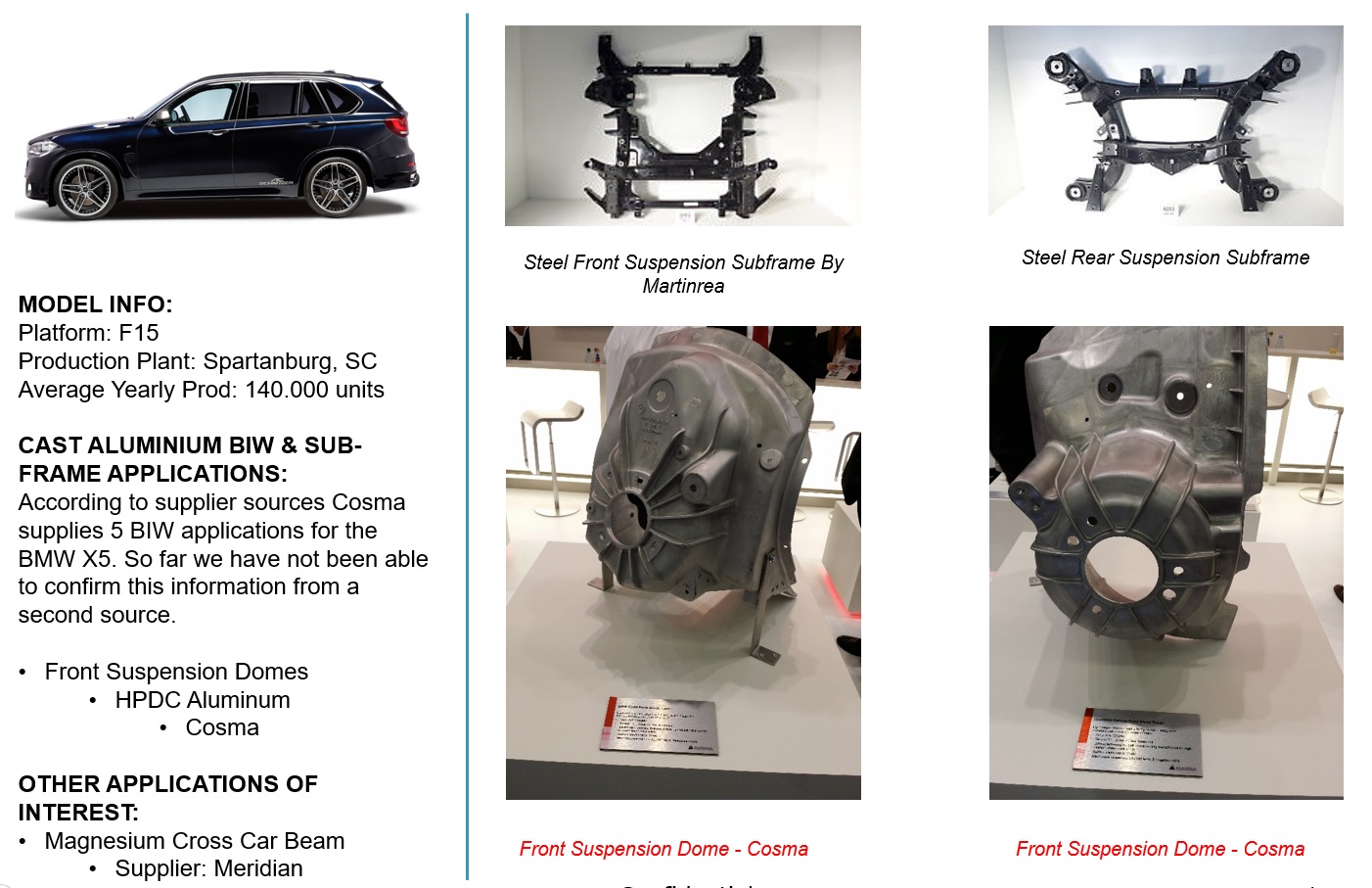

BMW X5 & X6 Light Weighting by Material Suppliers – Source ALUMAG®

THE CLIEN REQUESTED SUPPORT FROM ALUMAG® TO EXECUTE THE FOLLOWING SERVICES & ANALYSIS:

Leading cast aluminum structures supplier for body and chassis parts

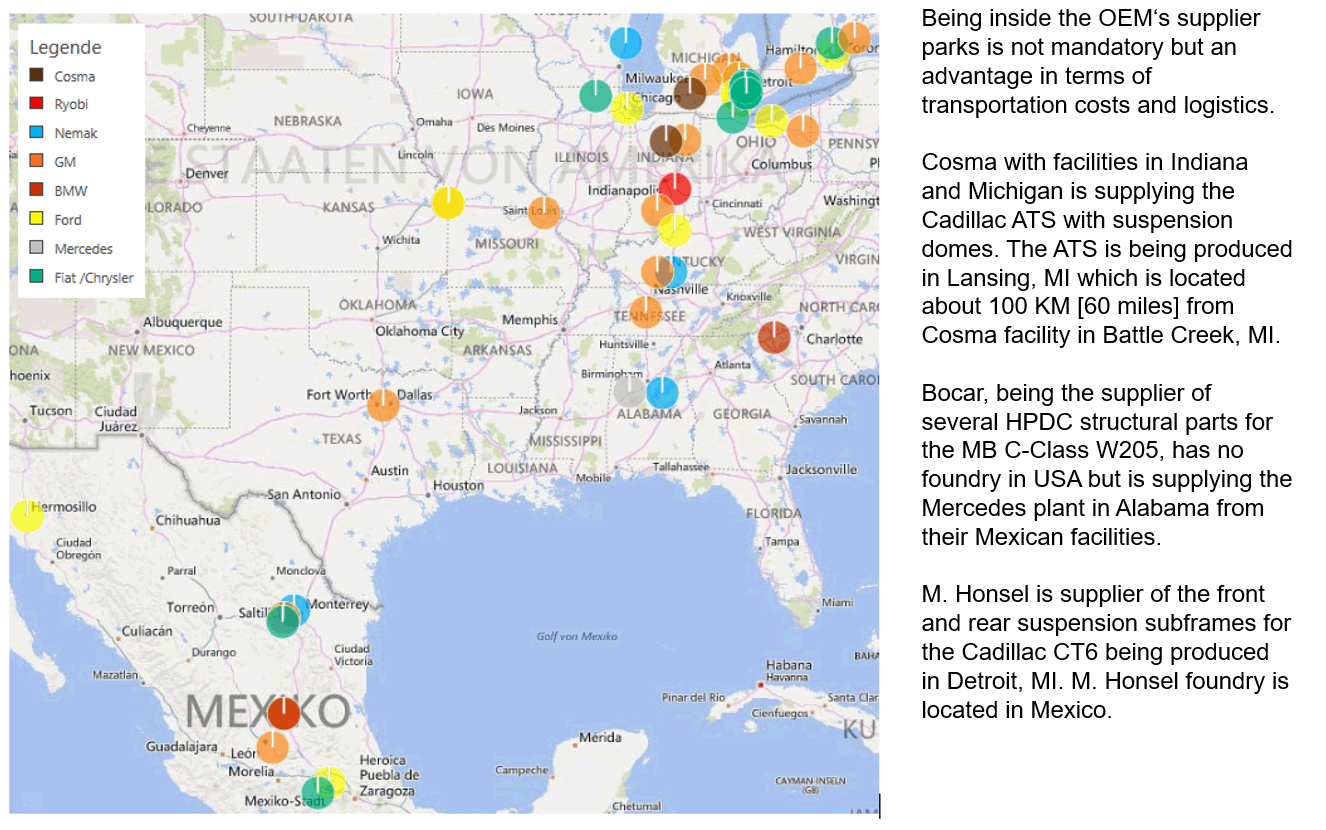

Selected car manufacturer in NA with their in-house casting, future strategy and make or buy decision as well as decision maker

Body and chassis segment NA, strategy, locations, expansions, supplier selection process and risks at selected car manufacturers

Market Research: ALUMAG Foundry Forging Company Database Incl. Giga-Casting Presses

ALUMAG Foundry Forging Company Database provides a comprehensive worldwide overview of 1500 foundry, forging & die-maker companies, including Giga-Casting Presses with all their capablities.

MARKET RESEARCH / DATABASE: BENEFITS

List of foundries & forgers incl. Mega-Casting , Hyper-Casting & Giga-Casting Presses

Search & validation for M&A targets [M&A module is optional]

Target client database for pro-active sales / new market & business development

Supplier database for casting & forging & moulds by region, materials,….

MARKET RESEARCH / DATABASE – INTRODUCTION: ALUMAG® as a provider of automotive forecasting, market research and databases, offers a new market intelligence database. The database lists die casting, forgers, die-makers, Mega-Casting Hyper-Casting as well as Giga-Casting Presses / companies for strategic localization tasks. The Giga-Casting Presses & Foundry Database [FDB] was created in 2014, causally for aluminum casting entities in NA. This local nucleus quickly developed into a global approach and implementation. Today, this is the only global comprehensive foundry presses company database.

Over the recent years, ferro & iron, forging and mold / die making companies/ presses have also been added to the database as well as a special focus on Mega-Casting, Hyper-casting & Giga-Casting Presses.

MARKET RESEARCH / DATABASE: DESCRIPTION & CONTENT – FOUNDRIES:

Full address with allocated filter for regions, countries and states.

Kind of locations, OEM or TIER, Plant or HQ

Share of cast aluminum, magnesium, iron or zinc.

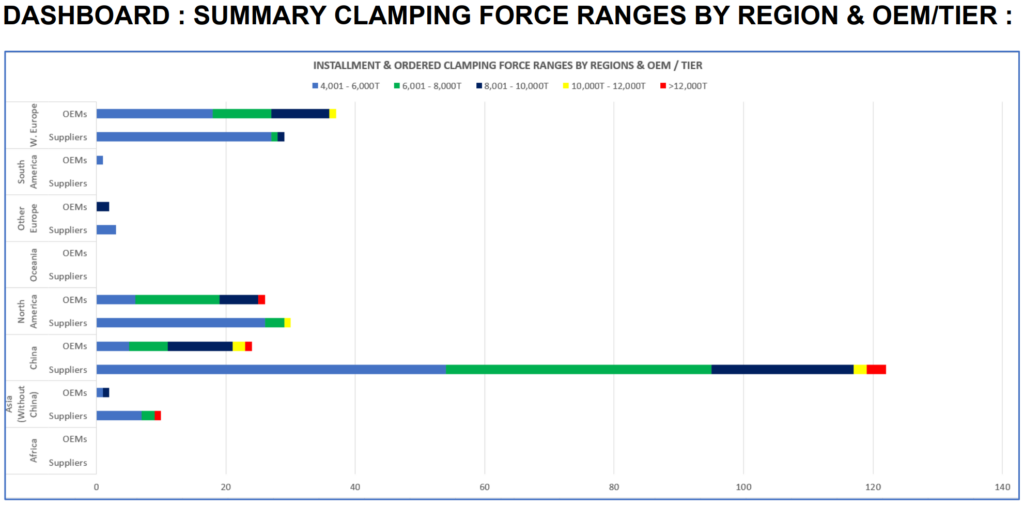

Clamping force range [HPDC] up-to 20NM / 20,000 tons.

Number of casting cells/ presses by clamping force ranges for HPDC [note pic below].

Further inhouse casting processes like SC, GDC, LPDC, CPC, HPDC, HOLLOW etc

Pre & post cast processes, such as in-house engineering, die / tool shop [build or repair], vacuum, HT, CNC, leakage test, impregnating [sealing], assembly, …

Industries served : Aeronautics, Automotive, Energy, General Engineering, Marine, Medical, Military.

Cast applications and products in production by 22+ predefined product groups like ICE, E-Motor, BiW,

Special focus on Mega-Casting, Hyper-Casting as well as Giga-Casting Presses.

Reference customers.

Certifications ISO 9001, ISO 14001, IATF16949.

Incorporation, employees, shareholders, revenue [USD], capacities in units / tons.

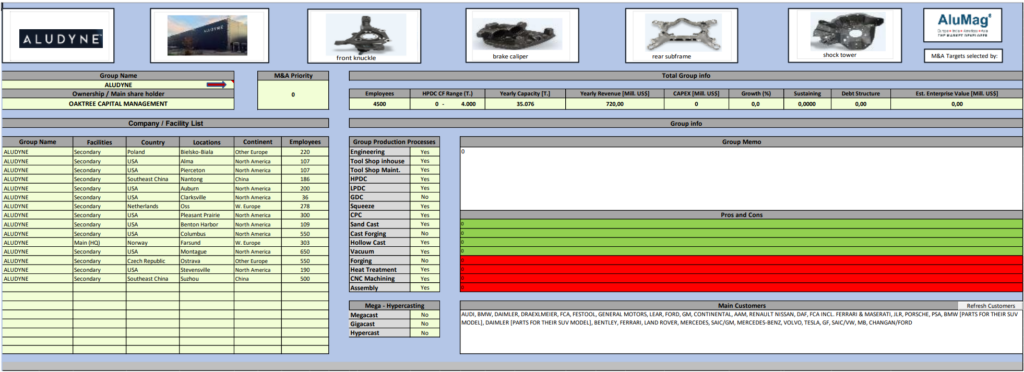

Facility List: List containing 1,360+ froundry facilities incl. the mentioned criteria by plant above.

Group Summary: 710+ group figures are summarized and calculated automatically based on the facility inputs for the 1,360+ facilities. Information available are :

Group Key figures [revenue, employees and capacity] in M&A module.

Group number of foundries by region [NA, SA, EU, Asia, China].

Group clamping force range & number of cells [HPDC] incl. dynamic graphics.

Group Pre & post cast processes [In-house engineering, tool shop [build or repair], assembly, heat treatment, CNC].

Group cast applications & products in production [22 predefined product groups].

Fact sheet: An overview of each inserted group showing all information available [Picture sample below]

MARKET RESEARCH / DATABASE: CUSTOMIZATION – ON REQUEST POSSIBLE On request ALUMAG® will complete the insertion of data for any existing or new requested database criteria into the market intelligence tool “ALUMAG Giga-Casting Presses, Forging & Foundry Database”.

With our extensive global network and comprehensive industry knowledge and knowhow, ALUMAG® is highly qualified to support global companies on cross border Mergers and Acquisitions. Depending on your inhouse resources and industry knowledge ALUMAG® is a qualified partner for any M&A localization projects or as a provider of market intelligence/ market research on which you could execute your own inhouse M&A analysis.

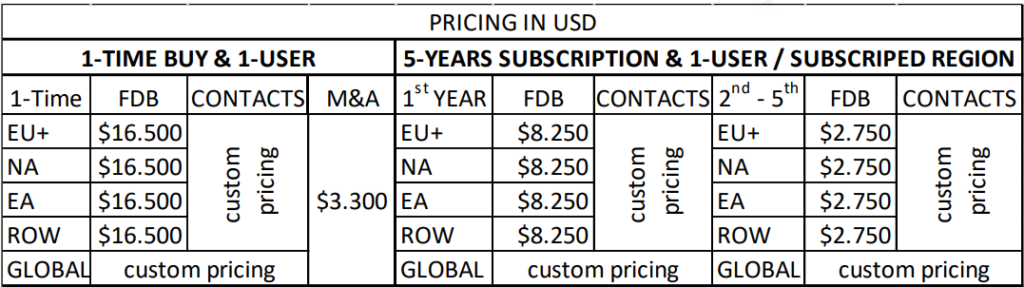

MARKET RESEARCH / DATABASE: PRICING

Example for a 5-years North America subscription & 1 user: 1st year = 7,740 €UR / 59,700 CN¥ / 140,000 MXN / 8,250 U$D / 1,274,000 ¥EN 2nd-5th = 2,580 €UR / 19,900 CN¥ / 46,660 MXN / 2,750 U$D / 424,800 ¥EN

EU+ [European Union plus the countries: CHE, GBR, SRB, TUR]

NA [CAN, MEX, USA]

EA [East Asia with CHN, JAP, KOR, MNG, TWN]

ROW [Rest of the World like, AUS, BRZ, IND, RUS, …, ZAF]

M&A: Prepared but blanked/unloaded “M&A module” incl spider diagrams [gathered and typed-in data by ALUMAG® on individual quoted clients demand].

ALUMAG POSTS & MARKET INFO RELATED TO GIGA-CASTING PRESSES:

OCT24 LINKED-IN POST BY JOST GAERTNER – ALUMAG CEO

The first Global GIGA-Casting Congress in Kassel on March 5th & 6th, 2025 is addressed to people from all over the world, who are interested in new GIGA-Casting developments and applications. The congress is hosted by the Chair for Foundry-Technology GTK at the University of Kassel in cooperation with ALUMAG Automotive GmbH. The congress offers an excellent opportunity for international exchange on topics relating on new GIGA-Casting technologies and strategies. Come to the first international GIGA-Casting Congress with excellent lectures from technology and strategy experts regarding the future for new automotive casting concepts and enjoy our Foundry-Evening with the wonderful atmosphere of the Alte Brüderkirche (Old Brother-Church) in Kassel !

AUG24 LINKED-IN POST BY JOST GAERTNER – ALUMAG CEO

In the middle and long run, the magnesium HPDC / die-casting components will cost less than in aluminum. The following reasons:

1. Magnesium mold / mould for the die casting / HPDC has upto 4x life time / # of shots.

2. Magnesium thixomolding will be even less expensive than thixocasting.

3. Beside thixocasting and -moulding, a third potential process is MAXImolding®.

4. China has its focus on magnesium, has produced app 1 Mill tons in 2023.

China progressively expanding its application in automotive, rail cars, 5G housings / heat sinks, ..

5. BAOWU, one of the super large steel group, has entered the market by an aquisition of five HPDC / Die Casting plants. Beside those, BAOWU owns the entire magnesium chain. According to sources, BAOWU holds or has its hand over 70% of the Chinese magnesium market

6. The USA has entered the market, too.

7. For comparatively cheap and environmentally friendly magnesium [including the draw out of further key minerals, such as lithium] from oceanwater as a by-product of the water desalination.

8. It is spoken of, in the mid run, the cost will be <1 U$D/1Kg magnesium raw materials to purchase.

Giga-Casting Presses will be one of the main equipment and process, to produce such large structural parts, beside formed sheet.

JULY24 LINKED-IN POST BY JOST GAERTNER – ALUMAG CEO

A LK 7000 tons clamping force HPDC / DCM / Megapress has been packed for its shipment to the Serbia plant. The large press will be operated by UAT [United Alloy Tech], the MINTH die casting division. Target automotive applications are HV battery trays / closures and large front and rear underbody structures.

Giga-Casting Presses will be one of the main equipment and process, to produce such large structural parts, beside formed sheet.

OCT23 LINKED-IN POST BY JOST GAERTNER – ALUMAG CEO

Lightweight construction is just one descriptive feature. Cast aluminum is much more, such as functional integration, component reduction, less effort for sealing and joining technologies, process simplification, stiffness and tightness. We will never again reach the volume of around 20 million vehicles produced in Europe, rather settling at 15 million annually, followed by less aluminum casting overall. With the reduction of PHEV market penetration, there will be a further reduction in the demand for aluminum casting, per vehicle and overall. A large number of AL cast CU and sensor housings are eliminated as they are centralized and partially replaced by plastic. BEVs have 15 to 20 kg less AL casting per vehicle due to the virtually elimination of the five- to eight-speed automatic transmissions in the powertrain alone. The growth in gigacastings and AL cast HV battery housing holders, transverse stiffeners, …., will not be able to replace the application reductions described above.

Connect with Jost GAERTNER at: https://www.linkedin.com/in/jost-gaertner-482b3328/

LIKELY ALSO OF INTEREST:

Please have a look at our automotive research tool ALUMAG GLOBAL AUTOMOTIVE SYSTEMS DATABASE [ASDB] E.G. This database provides detailed information for each automotive application in regards to model, platform, material, process, weight etc. Listing also Giga-Casting applications.