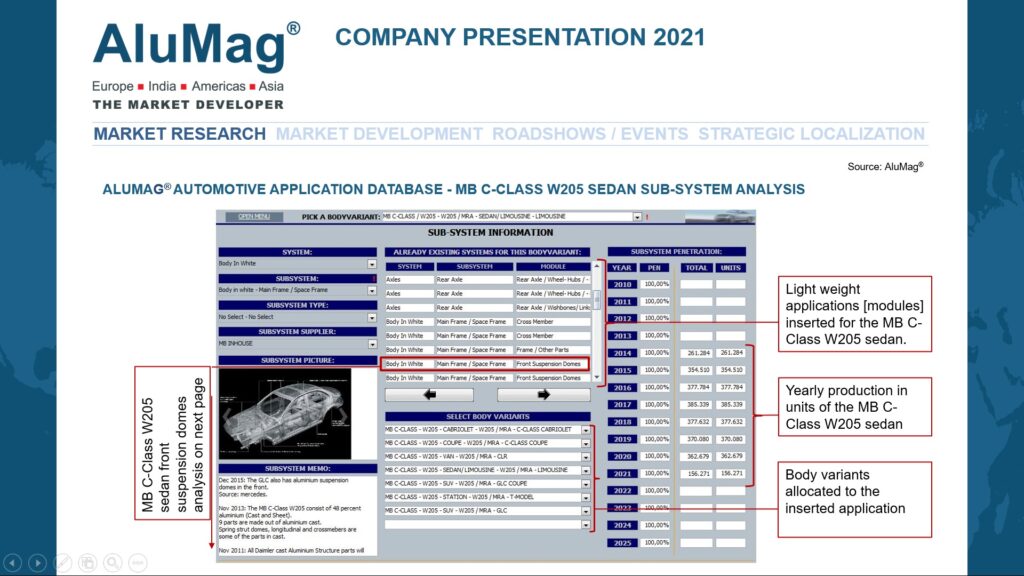

Automotive Lightweight Application Database

Data Sample: Automotive Application Database

Data Sample: Automotive Application Database

Jost GAERTNER

Managing Partner

Contact Details

Tel: +49 172 6000569

j.gaertner@alumag.com

Ying ZHOU

Lead Of Japan & China Projects

Contact Details

Tel: +49 172 6415876

y.zhou@alumag.com

DATABASE DESCRIPTION:

The database contains details regarding around 10.000 automotive aluminum, magnesium, steel & CFRP applications by car body variants (Supplier – Material – Process – Weight – Demand By Bodyvariant)

TREND ANALYSIS:

The Automotive Application Database is connected with ALUMAG® in-house automotive production forecast. Accurate material demand analyses by model variant are generated by multiplying an application weight with yearly model variant production.

The direct connection with our automotive production forecast makes it possible to generate several data enquires:

- Demand by material [aluminum, magnesium, steel, composite, carbon]

- Demand by core processes [cast, extruded, rolled, forged, …]

- Demand by OEM

- Supplier market shares

- Demand by application