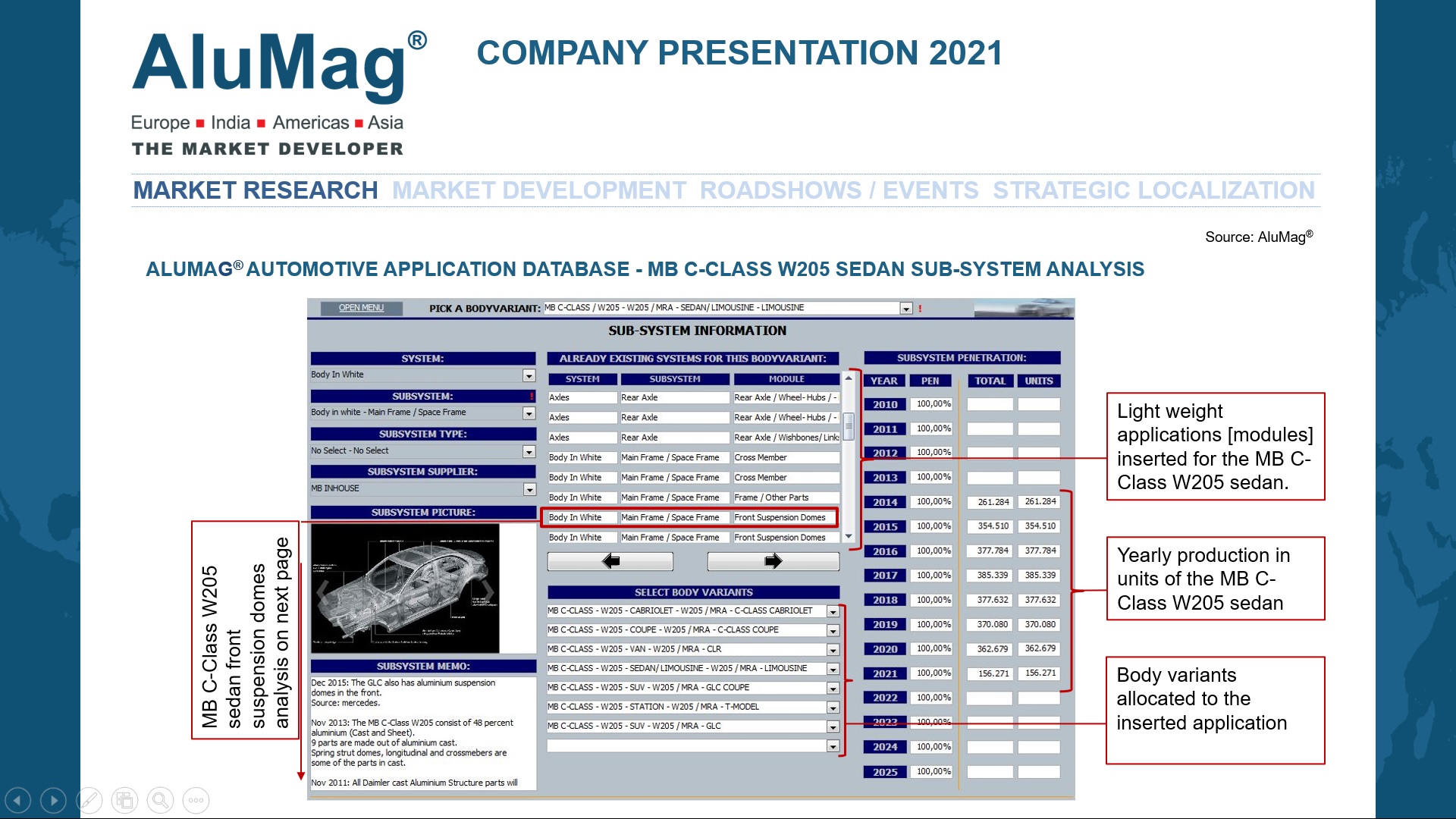

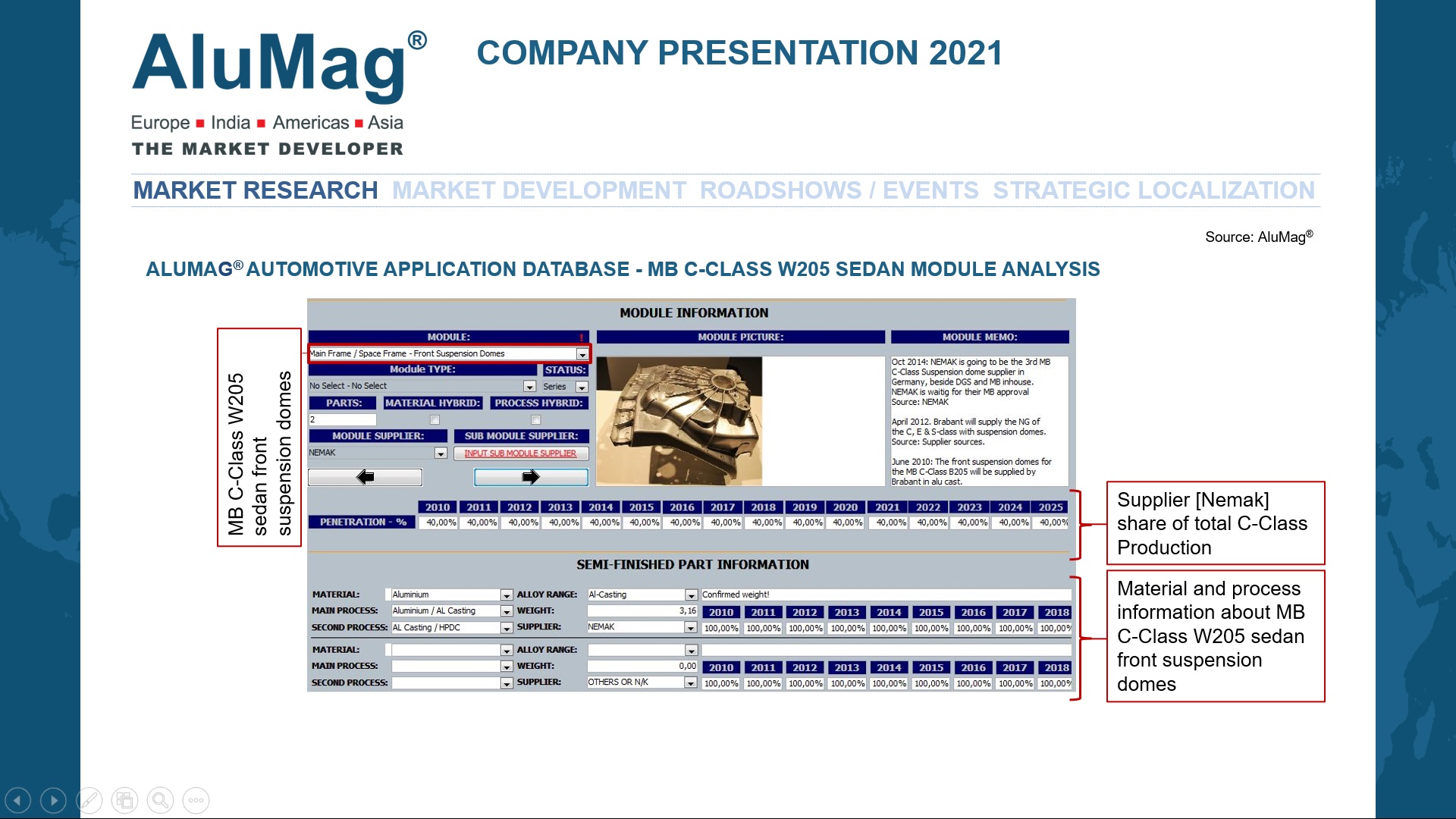

The database contains details regarding around 10.000 automotive aluminum, magnesium, steel & CFRP applications by car body variants (Supplier – Material – Process – Weight – Demand By Bodyvariant)

TREND ANALYSIS:

The Automotive Application Database is connected with ALUMAG® in-house automotive production forecast. Accurate material demand analyses by model variant are generated by multiplying an application weight with yearly model variant production.

The direct connection with our automotive production forecast makes it possible to generate several data enquires:

Demand by material [aluminum, magnesium, steel, composite, carbon]

Demand by core processes [cast, extruded, rolled, forged, …]

Power train: EV battery trays/ housings, EV Motors

–

SYSTEM DATABASE – CASE: EU27+ ANALYSIS: BEV MARKET INTELLIGENCE : AL PROCESSES – APPLICATIONS – SUPPLY CHAIN

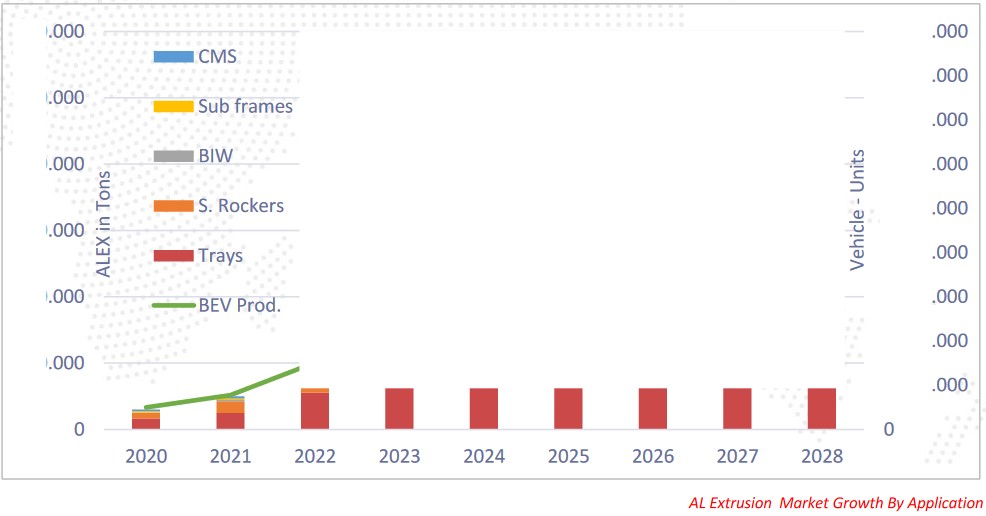

The market intel provides a basic understanding, technical / cost insights and demand overview of the market for multi hollow extruded aluminum sections.

In course of the market intel around 150 current and future BEVs were analysed in regards to material use in key structural applications such as BIW parts, CMS, HV battery frames/trays, side collision rocker and subf rames.

And, with the EU27+ BEV penetration forecasted to grow form 10% in 2022 to 41% in 2028, prospects for BEV applications are looking good. Though only HV battery frames and side collision rockers are obviues BEV components, BIW, sub frames and CMS are equily interesting in this context as their specs are partly redefined in BEVs.

The bottom-up intelligence of the 150 BEV models revealed some interesting but not expected facts. Extruded aluminum is and will play a dominant role within structural BEV applications [CAGR of 64%] in the timeframe 2020 – 2025.

And while the MEB 1 platform by VW Group accounts for almost 50% of the entire AL-extruded demand in 2022, 65% of the market demand will be spilt by 10 major BEV platforms in 2028….

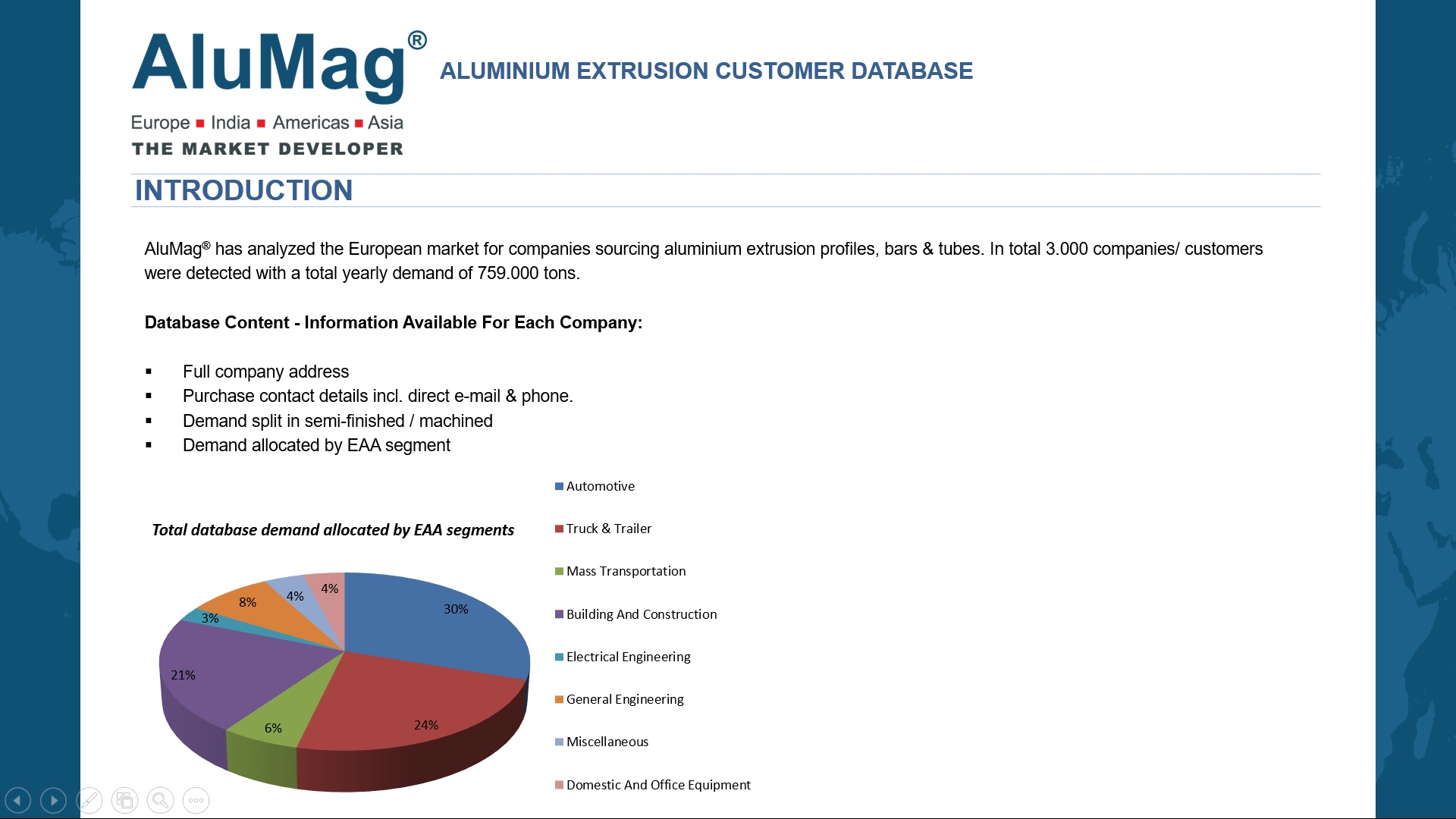

The ALUMAG® Aluminum Extrusion Customer Database is an acquisition tool containing about 3,000 companies, situated on the European market, and all with a demand for aluminum extrusion profiles/ tubes. The combined demand for the 3000 potential customer companies is about 755,000 tons aluminum extrusion profiles/tubes yearly.

All market segments have been analysed including automotive, truck & trailer and non-automotive segments like building & construction, furnitures, general engineering etc.

–

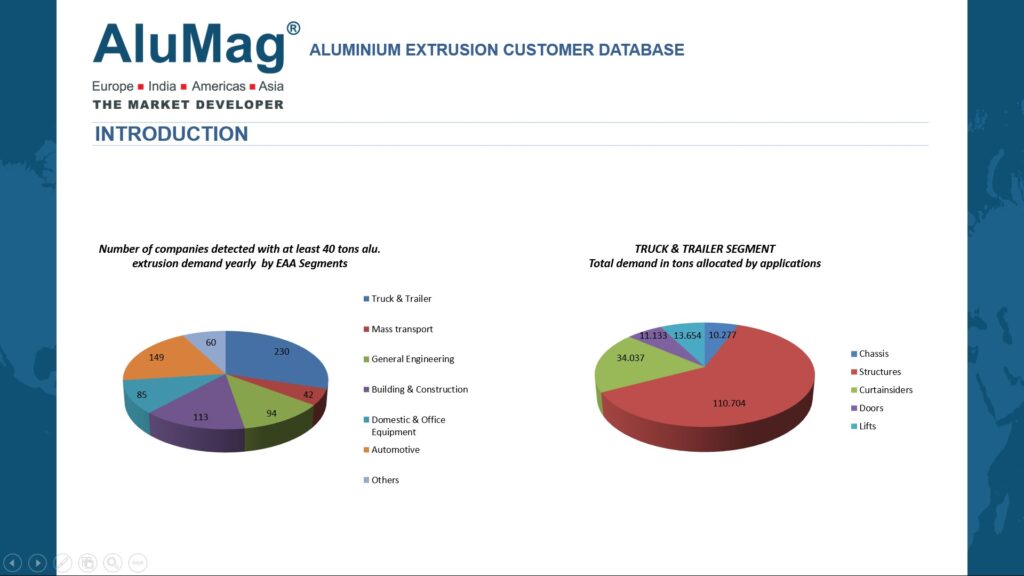

ALUMAG® Extrusion Database Details

–

For more information please download the presentation and/or contact ALUMAG® Automotive GmbH.

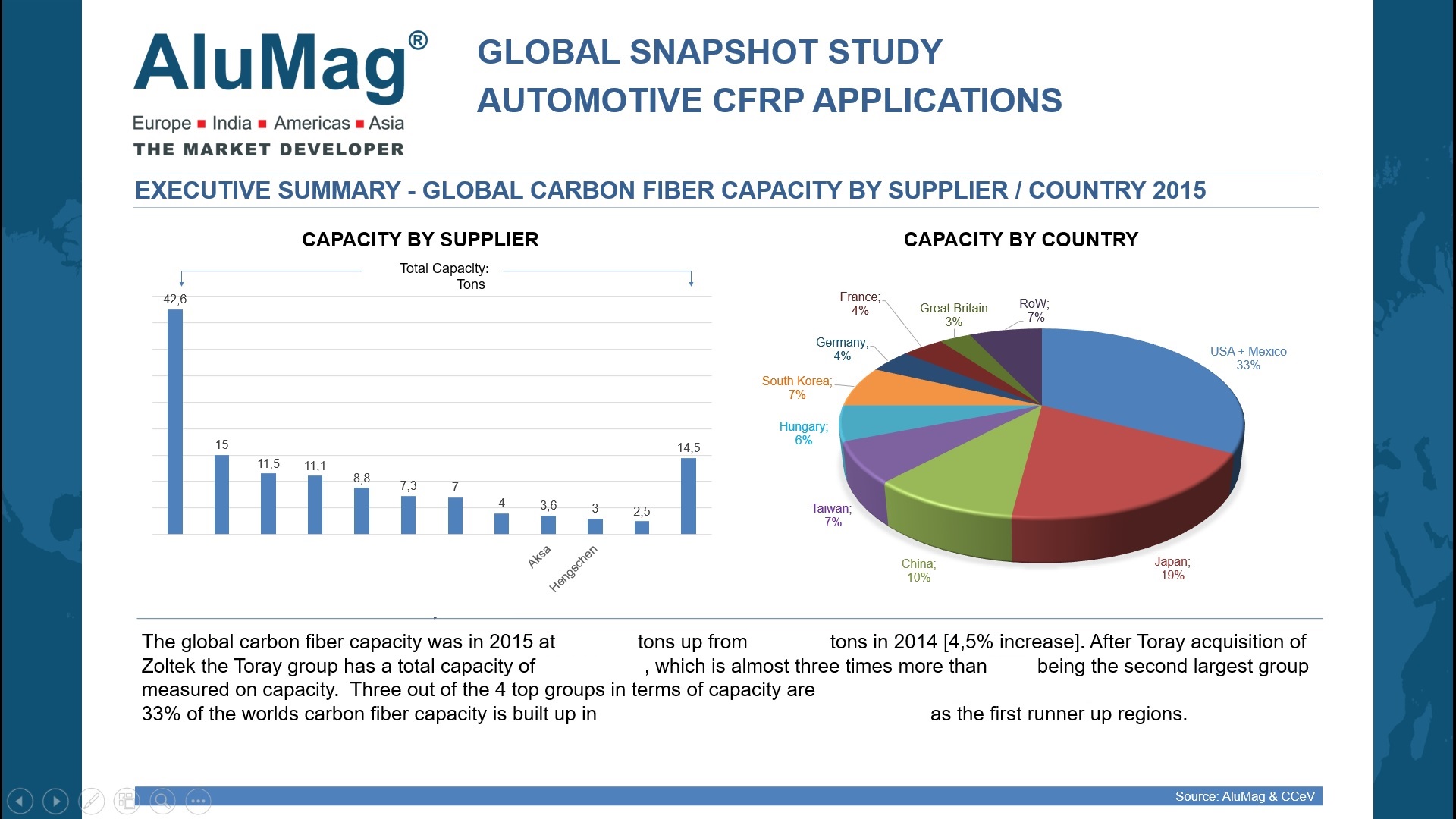

SCOPE & METHOD DESCRIPTION: For a Chinese producer of electronic equipment ALUMAG® executed a global snapshot study of the automotive CFRP market.

CFRP DEMAND & MARKET SHARES: ALUMAG® has analyzed the consumption of CFRP in automotive BIW applications worldwide. Furthermore supplier market shares for each application group were determined.

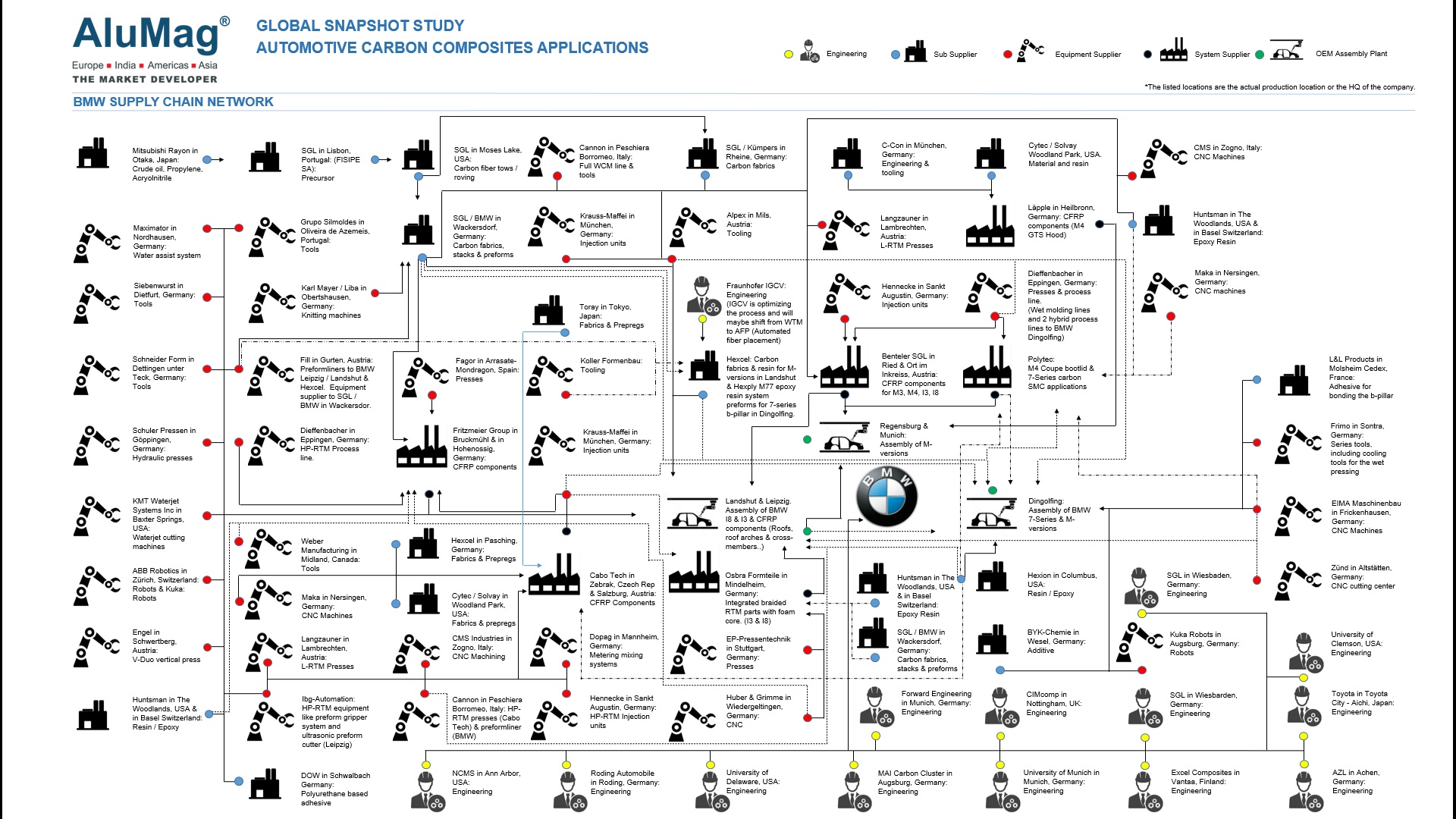

CFRP SUPPLY CHAIN: A comprehensive carbon fiber supply chain chart were researched for six premium OEMs. In total 110 companies were detected as being part of the six OEMs carbon fiber supply chain. For each company a qualified contact is listed

CFRP APPLICATION TECHNOLOGY OVERVIEW: As part of the analysis several CFRP BIW applications have been thoroughly described in regards to material, process steps, equipment and assembly.

–

BMW Carbon Fiber Supply Chain Network; Source ALUMAG®

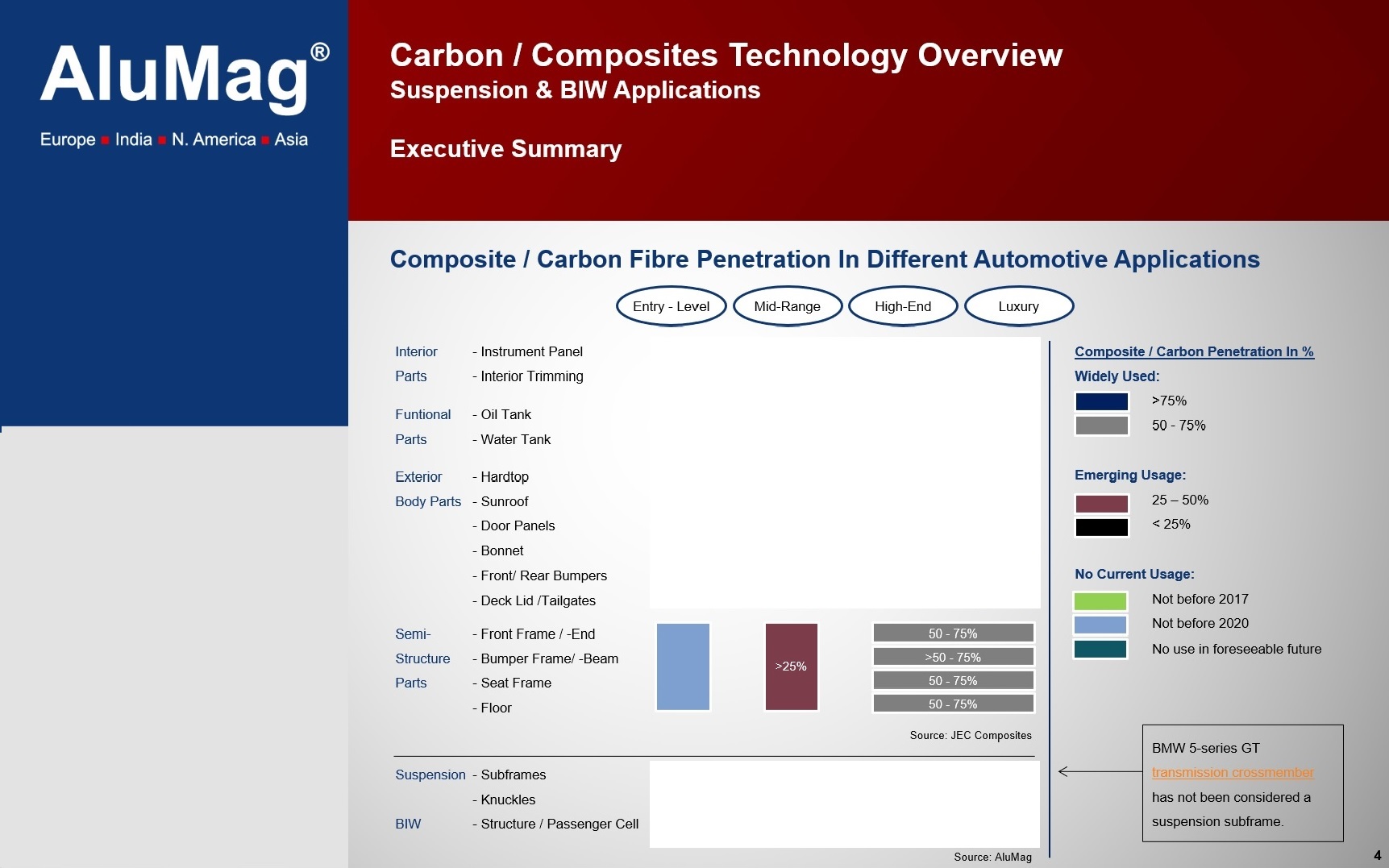

ALUMAG® has analyzed the composite / carbon fiber threat against cast aluminum within suspension and BIW applications.

The main goal was to provide the client [European aluminum foundry] with an application overview outlining the composite / carbon fiber threat by means of a timeline “What to expect when”.

The timeline was based on existing ALUMAG® market information as well as on 20 interviews with industry experts representing OEMs, carbon fiber producers and tool makers.

–

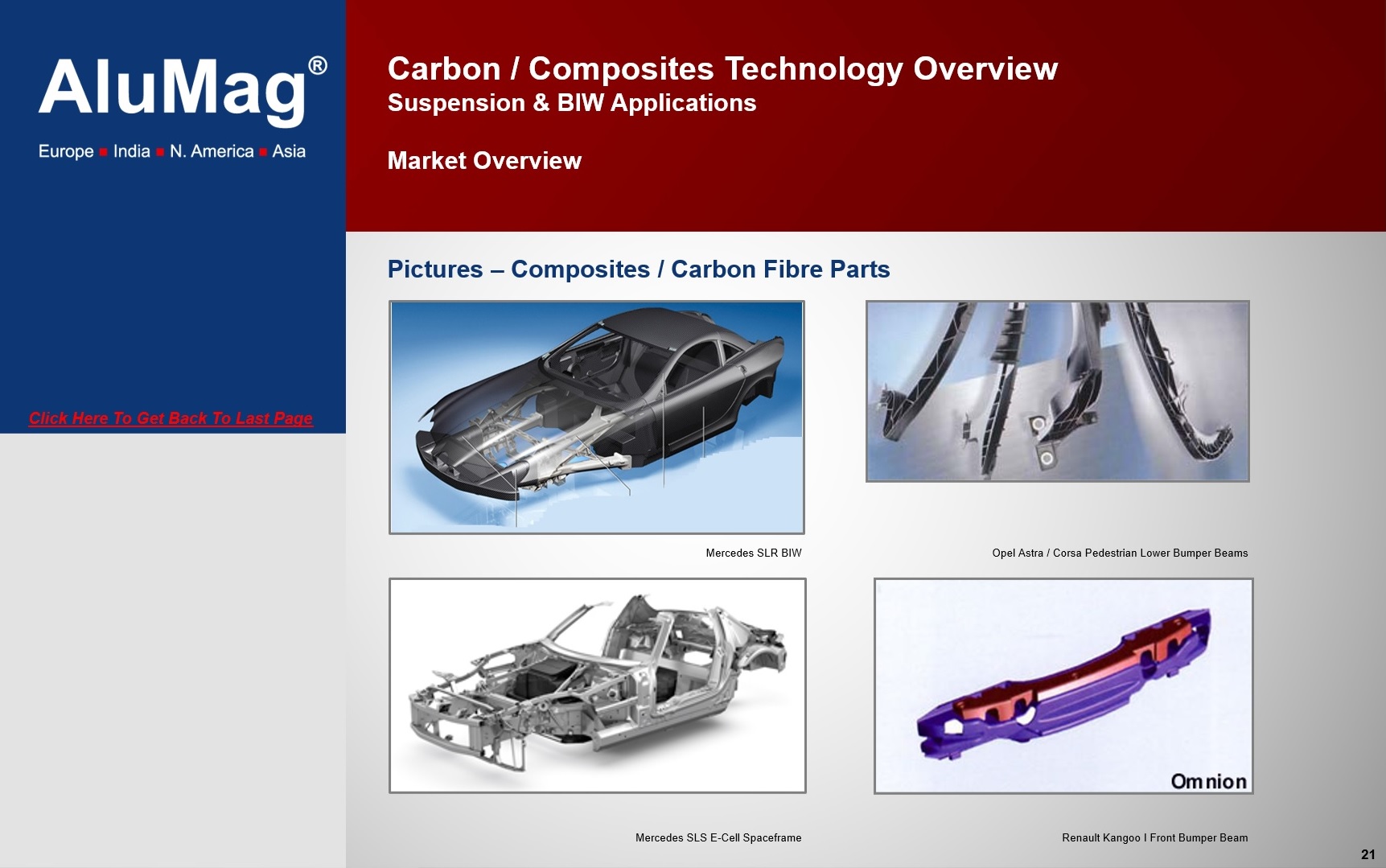

Samples of composite / carbon fiber automotive applications, source ALUMAG®

Cast aluminum is primarily used in power train applications, such as cylinder heads, engine blocks and transmission housings. In NA about 85% of all vehicles are equipped with an aluminum engine block. In Europe, this figure is 55%, 60% in China and 45% in Brazil [2015]. For 2020, a penetration rate of 89% in NA is expected.

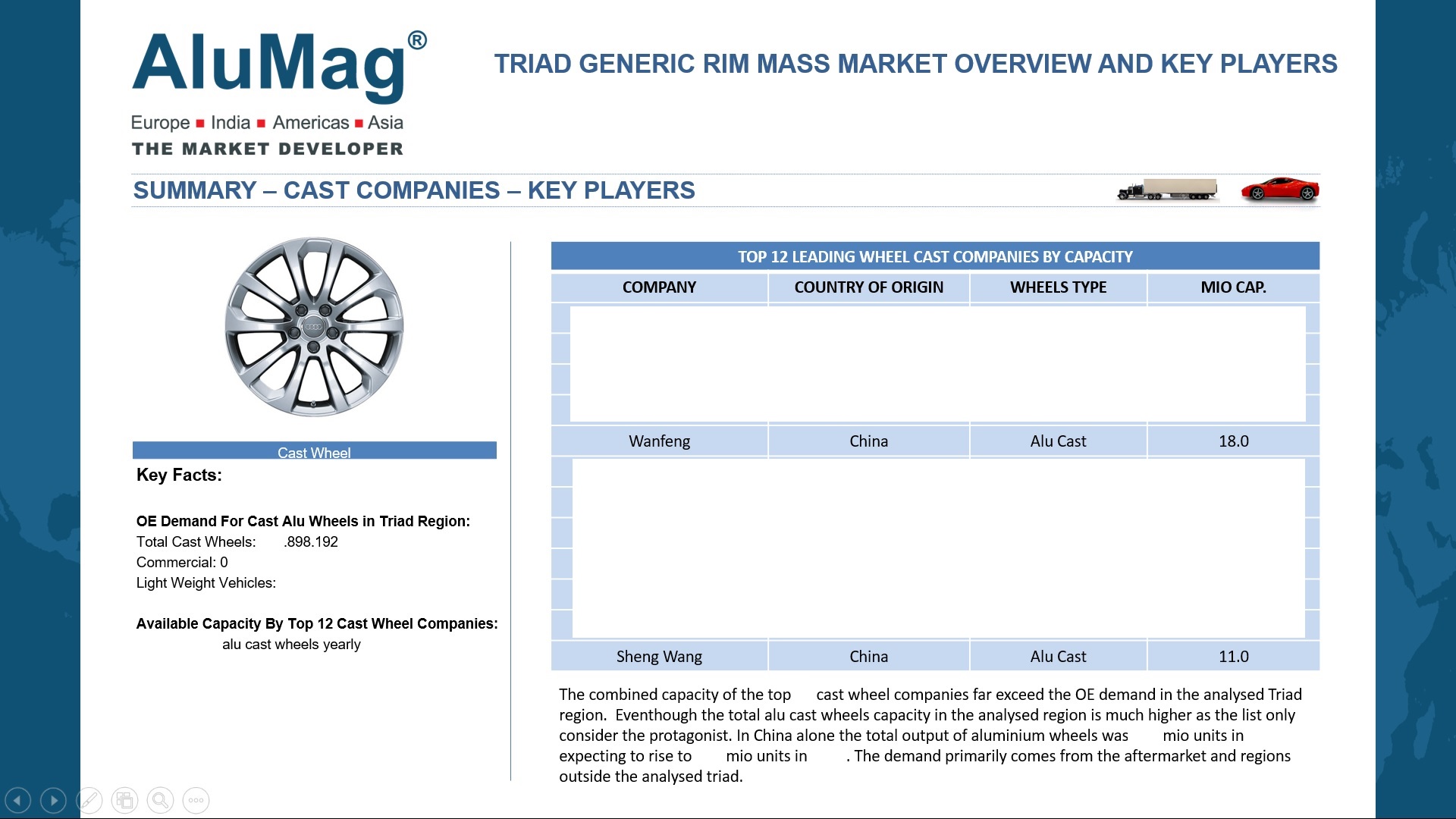

Another important application is cast aluminum wheels, currently around 45% of all vehicles sold are equipped with original cast aluminum wheels world wide. In NA, the OE incorporation rate is of 77% [2015]. For 2025 OE penetration rate of 50% is expected worldwide.

When it comes to BIW structures, especially sports cars are equipped with cast aluminum [vacuum HPDC] since the 90s. Audi initiated the turn with the introduction of an aluminum frame for medium to high Volume vehicles [A8 and A2] beginning of this millennium. The Audi “space frame“ Was made of cast-, extruded- and sheet aluminum processed parts. With a very high growth rate of applications in the automotive structure, aluminum is no longer a rarity. New generations of models of high-end car manufacturers such as MB [C,E, and S-Class], BMW [X5, X6, 5 & 7-Series], JLR [Range Rover, Range Rover Sport, XJ, F-Type, XE] Cadillac [ATS, CTS, CT6], Audi [Q7, A4, TT, A8, A6] have ..

–

AL Cast Market Summary & Outlook NAFTA – Source ALUMAG®

Worldwide the market for OE aluminum wheels is expected to grow with 0,91% in the period 2014-2015 within light weight vehicles. From 44% in 2014 to 45% in 2015. In the period 2014-2029 a growth rate of 7% points is expected which will bring the worldwide penetration of OE aluminum wheels up to 51% in 2029. The Highest growth rates in the period 2014-2029 are expected in China [14% points], Japan [13,5% points] and Central Europe [15% points].

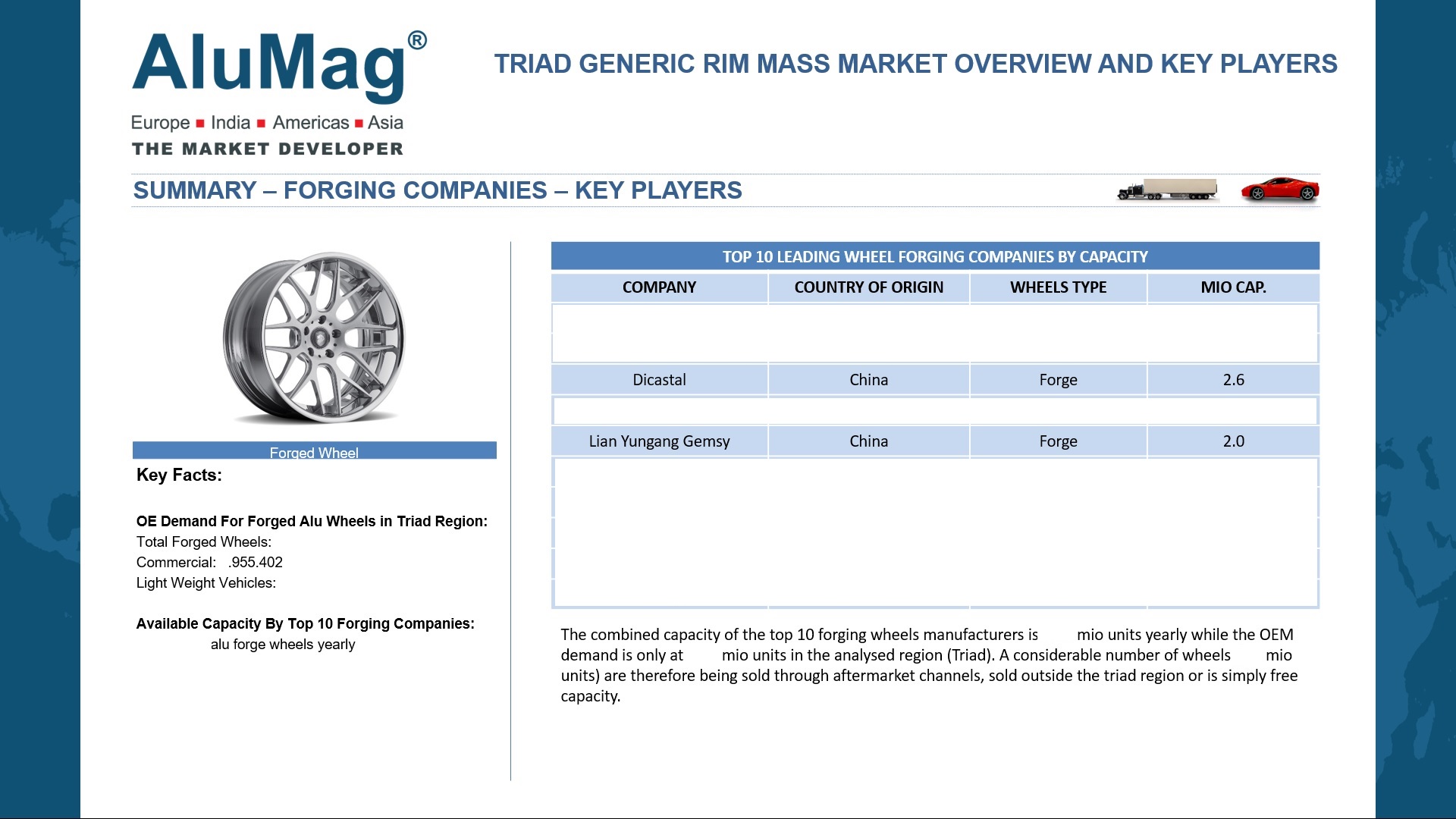

Cast wheels will remain the preferred alloy wheel for light weight vehicles while the penetration of forged wheels is expected to grow moderate over the coming years.

Today forged wheels are primarily used on high end vehicles and sports cars, but the booming electric vehicle segment Could boost the penetration of forging wheels in the near future. On the other hand new hybrid wheels to be launched by Maxion / Thyssen could become a threat to forging wheels manufacturers.

The penetration of forged wheels within commercial vehicles [Medium – heavy duty trucks, trailers and buses] is 13% on average in the analyzed regions. Again Nafta is the market with the highest penetration rate of forged wheels with 40%. Trailers and trucks in Nafta has in general more axles compared to other regions,..

Study was executed in year 2016/2017.

–

Global Forged Alloy Wheel Market Summary/Outlook – Source ALUMAG®